Have you ever wondered if you ended up with a fair deal on your mortgage? How do you know what interest rate you should be paying?

Even if you are confident in your current deal, how does your mortgage compare now that the Reserve Bank cut interest rates to historically low levels?

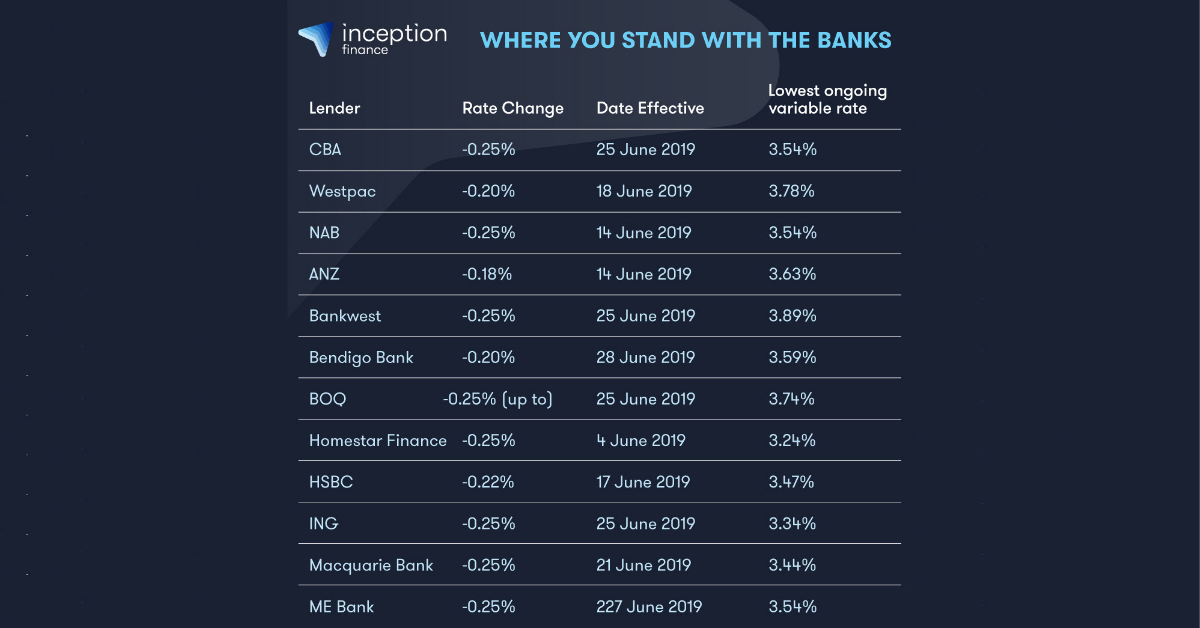

With the RBA’s decision to cut the money market “cash rate” you would think that consumers could expect to see this change, from 1.5 per cent down to 1.25 per cent reflected in mortgage rates, but dependent on your bank this may not be the case.

While a 25 basis point reduction in the cash rate may not seem like a huge move, for a typical $400.000 mortgage this could save anywhere between $60 and $720 in just one year.

Most Australians have a mortgage with one of the Big Four where what is known as a “discounted variable rate” is most common, which can seem like the best product, just based on the name – it’s “discounted”, right?

Well if you are an owner occupier and you’ve been paying off your home for some time, it may actually be better to look at a “lowest variable rate” offer instead which can be 1 percentage point lower than discounted variable rates!

Before the rate cut, the big banks lowest variable rates sat around 3.8 percent but now after the change there are rates as low as 3.54 percent being offered, which can make all the difference if you are really looking to get ahead.

For those of you on the fastest path to paying off their house, an offset facility is probably high on your priority list when looking at loans and while the big banks believe you’ll need to pay more for such accounts if you shop around you can often end up with a very similar rate but still have the benefits of the offset.

So, should you consider switching banks?

Our treasurer, Josh Frydenburg says you should shop around if you aren’t happy with the rate you are being offered by your current lender, a statement which was backed up by the Productivity Commission’s findings, showing that often banks will offer lower rates to new customers whilst charging higher rates to existing customers.

If you want to stay with your bank, consider researching first – find out the rate you’re paying, check what your bank is offering new customers and check what competitors might offer you.

ASIC make tools available online to help you understand the total costs involved with your current mortgage, and what it costs to switch. If you aren’t a big fan of crunching the numbers, talk to an Inception Finance broker and we can take the hard work out of finding the most competitive rate available on the market.

It is worth noting that after the banking royal commission, serviceability requirements have tightened and the application process has been slowed but if you have a strong history of paying down your mortgage things are generally quite simple as banks are always looking for high quality credit.

You may be wondering when the best time to look at a new rate would be as some banks will not reflect the change until the end of June, well that time is now!

So, If you are concerned about paying too much for your mortgage, start putting together your paperwork and crunching the numbers or - speak with an Inception Finance broker today about which steps you can take right now to ensure you are paying the right amount of interest on your loan.